The Ultimate Guide to NPS Tier 1 vs Tier 2: Tax Benefits, Withdrawal Rules & Which One You Actually Need

Planning for retirement is no longer a luxury; it is an absolute necessity. With inflation rising and life expectancy increasing, building a robust retirement corpus requires discipline and the right financial instruments. One of the most effective, government-backed wealth creation tools available to Indian investors is the National Pension System (NPS).

Governed by the Pension Fund Regulatory and Development Authority (PFRDA), the NPS is designed to help you accumulate wealth during your working years and provide a steady income after you retire. However, when you decide to start your NPS journey, you are immediately faced with a choice: NPS Tier 1 vs Tier 2.

Understanding the fundamental difference between NPS Tier 1 and Tier 2 is crucial because they serve completely different financial goals, have distinct tax implications, and follow completely separate withdrawal rules.

In this comprehensive guide, we will explore the nuances of both accounts, decode the tax benefits, and help you decide which account aligns with your financial strategy. Ready to secure your future? You can easily open an NPS account right now through the midfin360 app.

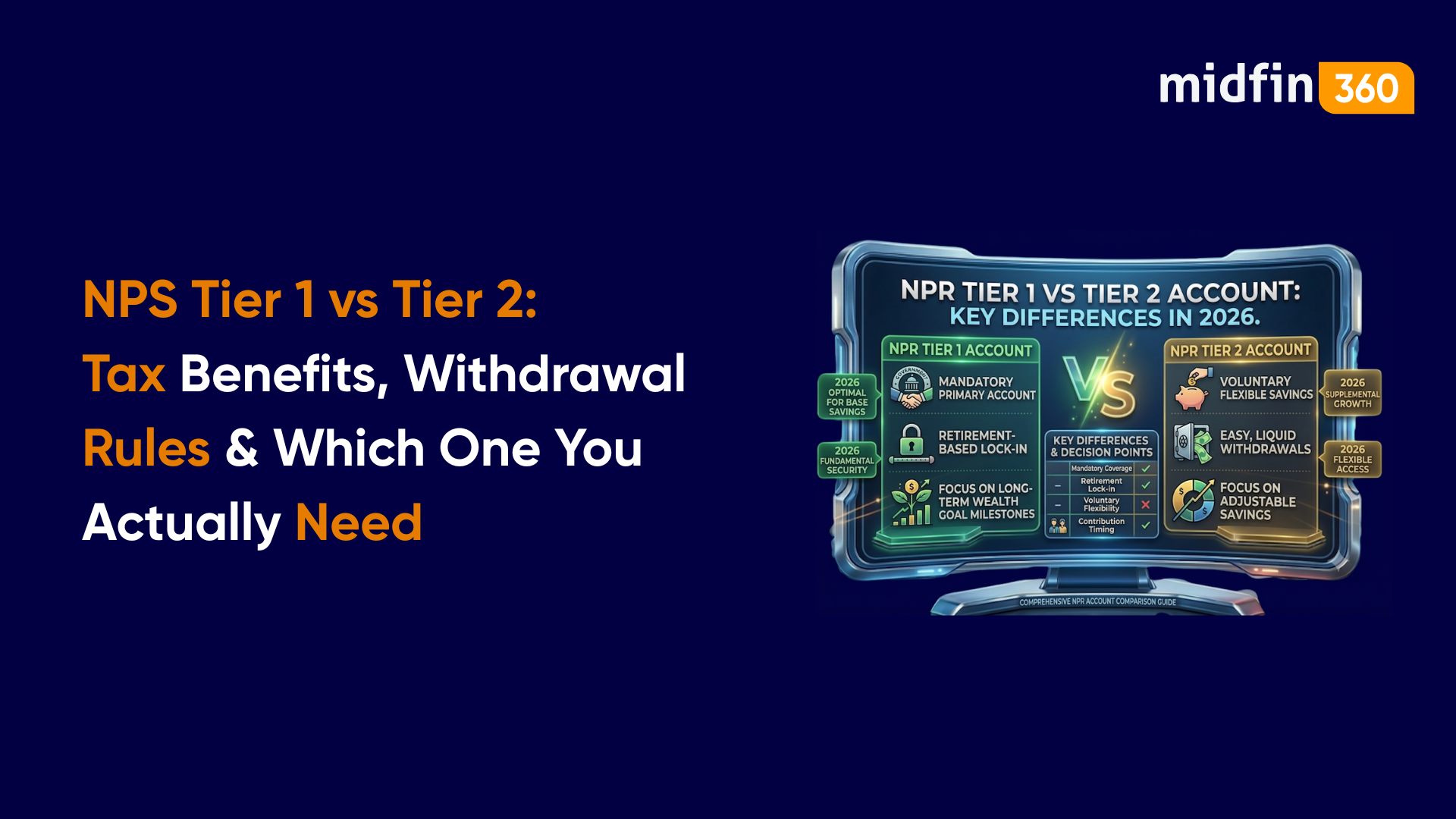

What is the Difference Between NPS Tier 1 and Tier 2?

Before diving into the complex regulations, let's establish the foundational difference between NPS Tier 1 and Tier 2.

Every subscriber who joins the NPS is allotted a unique 12-digit number called a Permanent Retirement Account Number, or PRAN. Your PRAN acts as the master key to your NPS identity, regardless of which tier you invest in.

- NPS Tier 1: This is the primary, mandatory retirement account. You cannot participate in the NPS without opening a Tier 1 account. It comes with strict lock-in conditions designed to ensure you don't dip into your retirement savings prematurely.

- NPS Tier 2: This is a voluntary investment account attached to your PRAN. You can only open a Tier 2 account if you already have an active Tier 1 account. It acts more like a standard investment vehicle with high liquidity and no mandatory lock-ins for regular investors.

To fully grasp how these accounts function, we need to look closer at their specific rules regarding liquidity, taxation, and investments.

NPS Tier 1 Lock-in Period and Withdrawal Rules

The most significant defining feature of the Tier 1 account is its strict illiquidity. The government wants to ensure this money is preserved for your golden years.

The Standard NPS Tier 1 Lock-in Period

Your money in a Tier 1 account is locked in until you reach the age of 60 (or superannuation). It is not designed for short-term goals like buying a car or funding a vacation. You are committing to long-term compounding, where your returns generate their own returns over decades.

NPS Annuity Rules at Retirement

When you hit 60 and your account matures, you cannot simply take all the money and walk away. The withdrawal rules mandate that:

- You can withdraw a maximum of 60% of your total accumulated corpus as a tax-free lump sum.

- A minimum of 40% of the corpus must be used to purchase an annuity from a PFRDA-registered life insurance company. This annuity provides you with a regular, taxable monthly pension for the rest of your life.

Note: If your total accumulated corpus at age 60 is less than ₹5 Lakh, you are permitted to withdraw 100% of it as a lump sum.

If you are nearing retirement, figuring out how to manage the lump sum payout alongside your pension is critical. For guidance on managing your post-retirement corpus, read our guide on building a retirement withdrawal strategy.

NPS Partial Withdrawal Rules

Life is unpredictable, and emergencies happen. PFRDA allows partial withdrawals from your Tier 1 account, but only under highly specific conditions:

- You must have been an NPS subscriber for at least 3 years.

- You can only withdraw up to 25% of your own contributions (not the employer's contribution or the returns generated).

- You can only make a partial withdrawal a maximum of 3 times during your entire NPS tenure.

- Approved reasons include higher education or marriage of children, purchase/construction of a primary residential house, or treatment of specified critical illnesses.

NPS Tier 2 Withdrawal Rules and Liquidity

If Tier 1 is rigid, Tier 2 is the epitome of flexibility. When comparing NPS Tier 1 vs Tier 2, the liquidity aspect is often the deciding factor for voluntary contributions.

Ultimate Flexibility

For the general public, there is absolutely no lock-in period for a Tier 2 account. You can deposit money and withdraw it on any business day, much like a savings account or an open-ended mutual fund. There are no exit penalties or limitations on the reasons for withdrawal.

NPS Tier 2 Lock-in for Government Employees (3-Year Rule)

There is one major exception to the "no lock-in" rule. Central Government employees can claim tax deductions under Section 80C for their contributions to a Tier 2 account. However, if they choose to claim this specific tax benefit, their Tier 2 contributions become subject to a strict 3-year lock-in period. For private-sector employees and self-employed individuals, this 3-year lock-in does not apply because they cannot claim 80C benefits on Tier 2.

Unpacking the NPS Tax Benefits Section 80CCD(1B) and Beyond

Taxes heavily influence investment decisions in India. When evaluating NPS Tier 1 vs Tier 2, the tax treatment of your contributions and your eventual maturity amount is vastly different.

Tier 1: The Tax-Saving Powerhouse

The Tier 1 account is highly prized for its incredible tax efficiency, governed by the Income Tax Department of India:

- Section 80CCD(1): Contributions up to ₹1.5 Lakh are eligible for tax deduction (this falls under the overall ₹1.5 Lakh umbrella of Section 80C).

- NPS Tax Benefits Section 80CCD(1B): This is the game-changer. You get an exclusive, additional deduction of up to ₹50,000 over and above the 80C limit. This pushes your total potential tax deduction to ₹2 Lakhs per financial year.

- Section 80CCD(2): If your employer contributes to your NPS (up to 10% of your basic salary + DA), that amount is also tax-deductible.

To make sure you don't miss out on claiming these deductions, it is crucial to stay updated on the ITR filing deadlines AY 2026-27.

NPS Tier 2 Taxation 2026

The tax rules for Tier 2 are much less forgiving.

- No Upfront Deduction: Unless you are a government employee utilizing the specific 3-year lock-in mentioned earlier, you get zero tax deductions for contributing to Tier 2.

- Taxation on Returns: The taxation of NPS Tier 2 returns in 2026 is a common point of confusion. Unlike equity mutual funds which enjoy favorable Long-Term Capital Gains (LTCG) rates, Tier 2 withdrawals are generally added to your annual income and taxed according to your applicable marginal income tax slab rate.

If you are looking for highly tax-efficient vehicles for your non-retirement wealth goals, you might be better off exploring tax-efficient fund categories within the regular mutual fund space instead of relying solely on Tier 2. Furthermore, if you are stuck trying to understand key jargon like Section 80CCD(1B) / expense ratio / STCG terms, we recommend bookmarking our glossary for easy reference.

Market-Linked Growth: Asset Allocation and PFM

Both NPS Tiers are market-linked products. They do not offer guaranteed returns. Instead, your money is managed by professional Pension Fund Managers (PFMs) registered with the regulator.

You have the flexibility to choose your own asset allocation across four asset classes:

- Equity (E): High growth potential, higher risk.

- Corporate Debt (C): Moderate returns, moderate risk.

- Government Securities (G): Highly secure, lower returns.

- Alternative Investment Funds (A): Available only in Tier 1 with a 5% cap.

The Equity Exposure Cap (75%)

To protect investors from excessive risk, the NPS enforces an equity exposure cap. Even under the "Active Choice" where you decide your own allocation, you can allocate a maximum of 75% of your funds to Equities (Asset Class E) up to the age of 50. After 50, this maximum equity limit tapers down by 2.5% every year.

Both tiers benefit from the power of Rupee Cost Averaging when you invest systematically every month. Because the NPS boasts an incredibly low expense ratio—often just a fraction of a percent—more of your money stays invested, boosting your long-term CAGR (Compound Annual Growth Rate).

NPS Tier 1 vs Tier 2 Which is Better?

The question isn't truly about which is "better," but rather which tool fits the specific job you are trying to do.

- Choose Tier 1 if: Your primary goal is building a retirement corpus, you want to forcefully lock away money so you aren't tempted to spend it, and you want to maximize your tax savings under Section 80CCD(1B).

- Choose Tier 2 if: You already have a Tier 1 account, you want a low-cost, actively managed portfolio for medium-term goals, and you require the flexibility to withdraw your money at any time without exit penalties.

However, before aggressively investing in Tier 2, it is highly recommended to compare it against regular mutual funds. Mutual funds offer a wider variety of schemes, dedicated fund manager guidance, better tax treatment for equity, and the ability to track performance metrics deeply. To understand the intricacies of fund performance, you can read up on Sharpe ratio, alpha, and beta.

For a direct, detailed breakdown of how Tier 2 stacks up against MFs, check out our dedicated analysis: NPS Tier 2 vs mutual funds.

Why Manage Your NPS and Wealth with midfin360?

At midfin360, we believe in a holistic, consolidated approach to wealth creation. We are a registered Mutual Fund Distributor (MFD) committed to guiding you through your financial journey.

When you use the midfin360 platform, you get:

- A Consolidated Portfolio View: Track your Regular Mutual Funds (SIPs, lumpsums), NPS contributions, and Fixed Deposits all in one single dashboard.

- Accurate Performance Tracking: Easily monitor the Net Asset Value (NAV) and calculate the precise XIRR (Extended Internal Rate of Return) of your investments.

- Goal-Based Guidance: As an MFD platform, we emphasize the value of regular mutual funds where you benefit from ongoing portfolio reviews, risk profiling, and alignment with your life goals—service and guidance that standalone direct platforms simply do not provide.

- Seamless Transactions: Execute NACH mandates seamlessly via NPCI infrastructure for automated monthly SIPs into your funds and voluntary contributions to your NPS. Complete your KYC digitally and securely.

Frequently Asked Questions (FAQs)

1. Can I open an NPS Tier 2 account without having a Tier 1 account? No. A Tier 1 account is mandatory. You can only open a voluntary Tier 2 account if you have an active PRAN linked to a Tier 1 account.

2. Are the returns in NPS guaranteed by the government? No. While the NPS is regulated by the PFRDA and is a government initiative, the returns are strictly market-linked. Your final corpus depends on the performance of the equity and debt markets and the asset allocation you have chosen.

3. What happens if I stop making voluntary contributions to my NPS account? To keep a Tier 1 account active, you must contribute a minimum of ₹1,000 per financial year. If you fail to do so, the account is temporarily frozen. You can unfreeze it by paying a small penalty and the minimum contribution. There is no minimum annual contribution required to keep a Tier 2 account active.

4. When comparing NPS Tier 1 vs Tier 2, which one allows me to save more tax? Tier 1 is the clear winner for tax savings. It allows for deductions under 80C, 80CCD(1B), and 80CCD(2). Tier 2 offers zero tax benefits for private-sector employees.

5. Can I switch my Pension Fund Manager (PFM) if I am not happy with the returns? Yes. You are allowed to change your PFM once every financial year. You can also change your investment choice (Active vs. Auto) and asset allocation multiple times a year, giving you control over your portfolio strategy.

6. Is the maturity amount from NPS Tier 1 completely tax-free? Partially. At age 60, up to 60% of your corpus can be withdrawn as a tax-free lump sum. The remaining 40% must be used to buy an annuity. While buying the annuity is tax-free, the monthly pension payout you receive from it will be taxed according to your income tax slab in your retirement years.

Conclusion: Start Your Wealth Creation Journey with midfin360

Choosing between NPS Tier 1 vs Tier 2 doesn't have to be a headache. Tier 1 is your strictly regulated, highly tax-efficient engine for securing a comfortable retirement. Tier 2 is a flexible, low-cost add-on that offers liquidity but lacks the tax advantages of its mandatory sibling.

For a well-rounded financial life, combining the long-term retirement security of the NPS Tier 1 with the wealth-generating power of regular mutual fund SIPs is a proven strategy. It ensures you are protected for the future while remaining agile enough to meet your current life goals.

Don't wait until retirement is knocking on your door to start planning for it. Start building your consolidated, diversified portfolio today with a trusted partner by your side.

Ready to take control of your financial future? Experience seamless investing, expert guidance, and total portfolio control in one place. Download the midfin360 app today and start your wealth creation journey!

Manage all from your mobile

Take charge of your finances seamlessly — only on the Midfin360 app